In the Markets Now: When To Diversify

A diversified portfolio is an acknowledgement that the biggest risks are typically the ones that no one sees coming.

Whether it is the three little pigs or the ant and the grasshopper (can you tell I have a 5-year old?), history is littered with parables extolling the wisdom of enduring short-term discomfort or irritation to prepare for bad times when things are good.

Diversification works the same way. By spreading one’s “bets” across a range of investments expected to act differently in different environments, investors can limit a portfolio’s drawdowns and smooth out the ride. Diversification acknowledges a simple reality: the future is uncertain, and even the most compelling investment ideas and smartest management teams can fail. Diversification is often called “the only free lunch in investing” because when done right, it can reduce portfolio risk and volatility without necessarily sacrificing long-term expected returns. Said another way, the diversified portfolio is built not for the forever-summer environment that we want, but for the winters that will inevitably come.

Of course, nothing is truly a “free lunch.” The downsides of diversification are clear from a behavioral viewpoint. In a strong and occasionally frothy bull market, prudence can feel somewhere between uncomfortable and downright miserable. In good times, investors are constantly tempted to pile into whatever is exciting and working best, whether it's AI stocks, SPACs, crypto, or something else. And, speaking from experience, if investors miss the boat on one theme, they begin a desperate hunt for the next (often even more speculative) thing, so as to not miss out on the fun twice. Whether these bets turn out to be good is almost irrelevant; the concentration itself leaves investors vulnerable to shocks. In an era dominated by indexing, concentration can develop automatically and even portfolios marketed as diversified can tilt toward a handful of market leaders.

Full disclosure: I’m still plenty bullish. This market is not over-extended (versus the historical average bull market) by length or size and is underpinned by strong profitability, policy tailwinds, and ample liquidity. But there’s a reason seasoned investors warn that “they don’t ring a bell at the top.” Most major peaks don't look dramatic in the moment, and most tend to occur amid rampant optimism. I’m not arguing for drastic action, but in my opinion, this is the time to take a closer look at your portfolio and ask probing questions. Am I as diversified as I thought I was? How did I feel during the recent market selloffs? Is my risk tolerance meter as tuned as it should be? Can I handle a big multi-year drawdown like the one Tech stocks saw in the early 2000s?

The challenge is that markets, like life, are inherently uncertain. Outcomes that seem obvious today were rarely obvious beforehand, and the biggest risks are typically the ones no one sees coming. A diversified portfolio acknowledges that reality. It accepts that some holdings will always feel unnecessary and that something will always be outperforming, just as the ant's food stockpile looked excessive before winter and the brick house looked overly expensive. But when winter arrives or the wolf comes knocking, that insurance looks less like a burden and more like a lifeboat.

In his book “The Most Important Things,” legendary investor Howard Marks wrote that “there are old investors, and there are bold investors, but there are no old bold investors.” An underappreciated truth in investing is that it’s not just about maximizing returns, it's about surviving long enough to enjoy them. Over a lifetime of building wealth, taking no risk opens the door to outliving one’s nest egg but taking too much risk (through concentrated holdings, unintended exposures, etc.) can lead to the kinds of portfolio drawdowns that are difficult to come back from. Diversifying is rarely exciting…but neither are the consequences of not diversifying a portfolio.

Index Definitions

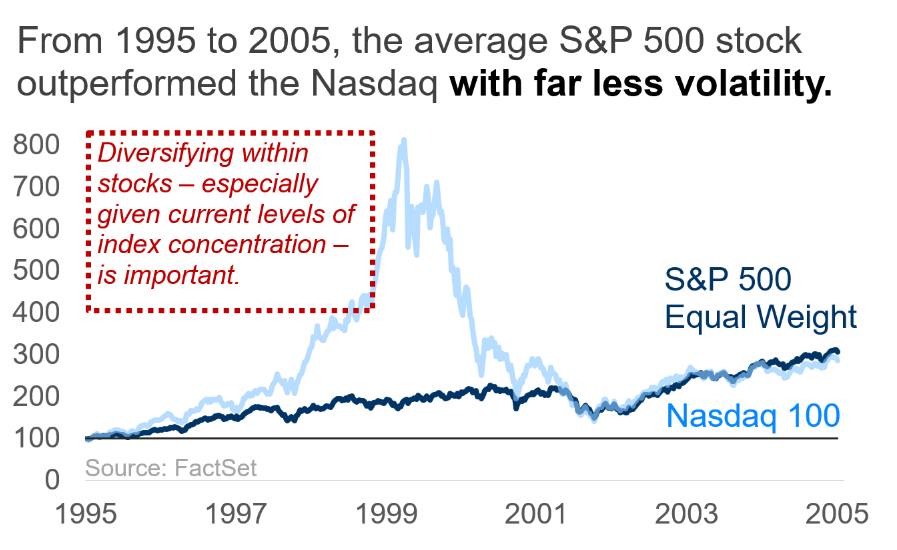

S&P 500 Equal Weight: An index that has the same large-cap, U.S. stocks as the S&P 500 but is often called the “average stock” because it removes the capitalization-weighting that allows a small number of large companies to have an outsized influence on the index.

Nasdaq 100: A tech-heavy, capitalization-weighted index of the stocks of 100 large non-financial companies that is dominated by major technology, biotechnology, and consumer names.

Disclosures

This is not a complete analysis of every material fact regarding any company, industry or security. The opinions expressed here reflect our judgment at this date and are subject to change. The information has been obtained from sources we consider to be reliable, but we cannot guarantee the accuracy. Market and economic statistics, unless otherwise cited, are from data provider FactSet.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation, or need of any particular client and may not be suitable for all types of investors. Recipients should not consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

For investment advice specific to your situation, or for additional information, please contact your Baird Financial Advisor and/or your tax or legal advisor.

Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Copyright 2026 Robert W. Baird & Co. Incorporated.

Other Disclosures

UK disclosure requirements for the purpose of distributing this research into the UK and other countries for which Robert W. Baird Limited holds an ISD passport.

This report is for distribution into the United Kingdom only to persons who fall within Article 19 or Article 49(2) of the Financial Services and Markets Act 2000 (financial promotion) order 2001 being persons who are investment professionals and may not be distributed to private clients. Issued in the United Kingdom by Robert W. Baird Limited, which has an office at Finsbury Circus House, 15 Finsbury Circus, London EC2M 7EB, and is a company authorized and regulated by the Financial Conduct Authority. For the purposes of the Financial Conduct Authority requirements, this investment research report is classified as objective.

Robert W. Baird Limited ("RWBL") is exempt from the requirement to hold an Australian financial services license. RWBL is regulated by the Financial Conduct Authority ("FCA") under UK laws and those laws may differ from Australian laws. This document has been prepared in accordance with FCA requirements and not Australian laws.